Wanting to own a beautiful, affordable luxury home is nothing new but what is new is the dramatic increase in mortgage rates which is tacking on thousands of dollars to the cost of purchasing a home. Americans are dealing with inflation on all ends of the economy spending more money on groceries, gas, and other everyday needs. Things are getting expensive and that’s obvious, but lots of folks don’t know just how expensive things are and what it might mean if you are in the market to purchase a home.

Mortgage Rates In 2022: What You Need To Know

Let’s go back to 2020 when things were somewhat normal before the chaos of COVID-19. Not only is the average home price up by more than 31% since June 2020, but mortgage rates since the latter half of 2022 have been steadily increasing as well. Mortgage rates were historically low at the beginning of 2022, hovering slightly above 3%, and then things took a drastic turn.

According to Freddie Mac, by the end of the first week, Jan. 6, 2022, the 30-year mortgage rate increased to the highest level since May 2020 to 3.22%, but it didn’t stop there. Rates continued on an upward hike landing us right around 5.89%.

You read that right. Since the beginning of this year, mortgage rates have shot up by almost 3 full percentage points and have even doubled since this time last year. As you can imagine, many people currently in the market to buy a home are starting to think twice and look into more affordable options -one being today’s more modern manufactured or modular home. The ability to get the same luxurious and spacious experience as a traditional home for a fraction of the price is practically a no-brainer considering the fact that rates are expected to continue to rise.

Which Market Factors are Affecting Mortgage Rates?

Many factors are affecting the mortgage rates in 2022. These include Inflation, the health of the economy, and the Federal Reserve. Generally, when the economy is considered to be in good shape, we will see mortgage rates increase due to the belief that borrowers can afford it. Another driving force is the Federal Reserve which many of us are familiar with. While they don’t directly control mortgage rates, they do have quite a bit of influence because prime rates for mortgages traditionally follow the trend of federal rates.

A bond market is a financial market where participants can either issue new debt or buy and sell debt securities. Mortgage-backed securities are typically sold in the bond market which affects mortgage rates depending on their demand. When demand is high, mortgage rates increase and when it is low, they decrease similar to inflation.

Inflation

How does inflation influence mortgage rates? Inflation and mortgage rates go hand-in-hand. When inflation happens, the value of the dollar increases reducing purchasing power directly causing mortgage rates to increase. When inflation increases, people will also start to see prices increase and this fact remains the same for homes.

How does inflation influence mortgage rates? Inflation and mortgage rates go hand-in-hand. When inflation happens, the value of the dollar increases reducing purchasing power directly causing mortgage rates to increase. When inflation increases, people will also start to see prices increase and this fact remains the same for homes.

Right now, we are experiencing the highest inflation rate we’ve seen in four decades! You’ve felt the sticker shock at the pump, the grocery store, and even your favorite restaurant. The annual inflation rate for the United States peaked in June at 9.1%, making it the largest annual increase since November 1981. In September, we are hovering at 8.3%. You can check out the inflation calculator chart to see current and historical US inflation rates here.

Health of the Economy

High inflation is a signal of an overheated economy. Post-COVID, economic growth has accelerated rapidly. Demand for goods and products, including housing, has simply outgrown the supply available. The limited supply of products in high demand, like housing, forces suppliers to raise prices continually.

Mortgage rates vary based on how the economy is doing today and its outlook. According to the US Conference Board, while the country is currently not “in recession….a broad downturn in the economy is on the way,” largely due to inflation and high-interest rates.

With the pandemic’s declining economic impact, inflation running at 40-year highs, and the Fed planning four more aggressive hikes, interest rates could continue trending upward this year.

Mortgage rates aren’t likely to fall again until late 2023 – at the earliest, according to Businessinsider.

The Federal Reserve

When The Federal Reserve needs to tighten up the money supply, they raise the Fed rate. To combat inflation and reduce overall demand in the economy for housing, the Federal Reserve began raising interest rates. Mortgage Rates mostly fluctuated through the second quarter of 2022 until the Federal Reserve’s June hike to curb inflation. The Federal Reserve does not set mortgage rates, but they do influence them. For example, the day after the Federal Reserve changed its rates, mortgage rates began skyrocketing with the largest week-over-week jump of .55% since 1987.

Will Rates Continue to Increase his Year?

Experts from Freddie Mac and other industry leaders differ on whether mortgage rates will keep climbing through the year or level off.

Experts like, Businessinsider, say mortgage rates aren’t likely to fall again until late 2023 – at the earliest.

The prediction pointing to an upward climb is attributed to a healthier post-COVID economy with low unemployment rates, high inflation, and the Federal Reserve’s plan for four more aggressive hikes.

What Factors Will Determine Future Rate Changes?

When trying to predict what’s to come as it pertains to future rate changes, there are five major factors to consider – all of which have to do with supply and demand. We’ve discussed the impact that inflation, the bond market, economic health, and The Federal Reserve has on mortgage rates but haven’t really covered housing market conditions. When more homes are being built or offered for resale, the increase in home purchasing leads to an increase in the demand for mortgages and pushes interest rates upward. You’ve probably heard real estate investors and agents rave about how crazy the market is for sellers specifically but what about purchasers?

In order to turn the market around in favor of prospective home buyers, we would have to see higher yields in the bond market, an increase in money supply by the Federal Reserve, and a tremendous decrease in inflation, but experts don’t necessarily see it going this way.

How are Experts Predicting Future Interest Rates?

Economic experts rely heavily on politics, consumerism, and other factors to help make projections about what rates will look like in the future. As of now, consumers expect interest rates to continue to rise to 6.7% by 2023 and exceed that by nearly two percentage points by 2025. Experts have a slightly different take. Lawrence Yun, NAR’S chief economist predicts that “as the Fed raises interest rates, the mortgage market will simply yawn,” assuming a stabilization of about 5.5% into 2023. Whether we see numbers closer to 5.5% or 6.7%, the truth is that both are higher than what most people can afford.

How Does This Affect Your Decision to Buy a Home?

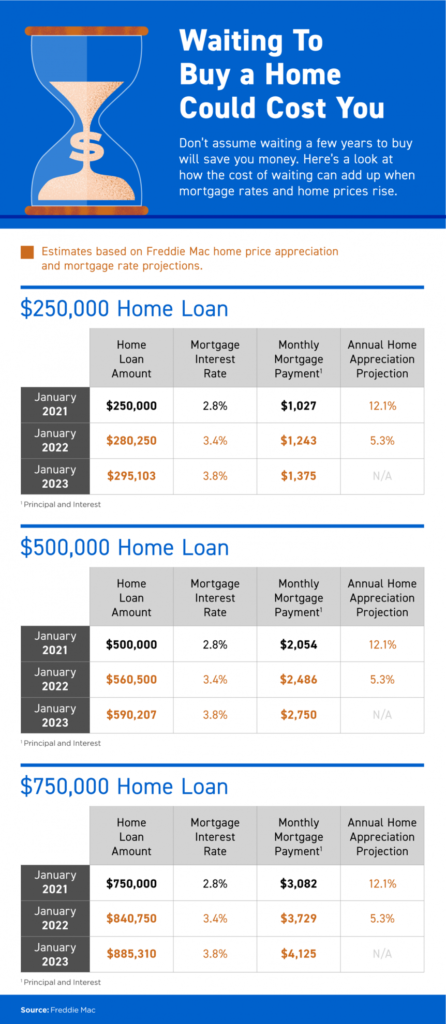

With rates being so high, families interested in purchasing a home are reconsidering based on affordability. Rising interest rates could raise your monthly mortgage payment and even fixed mortgage rates are more expensive. To put things into perspective (according to figures from NAR) a $429,000 house will cost an additional $5,640 per year. These additional costs are not small and prospective homebuyers are having a difficult time pulling the trigger on such an expensive decision but based on predictions, prices could continue to rise making purchasing a home sooner than later more ideal. Check out the chart attached with estimates on home costs based on Freddie Mac price appreciation and mortgage rate projections.

With rates being so high, families interested in purchasing a home are reconsidering based on affordability. Rising interest rates could raise your monthly mortgage payment and even fixed mortgage rates are more expensive. To put things into perspective (according to figures from NAR) a $429,000 house will cost an additional $5,640 per year. These additional costs are not small and prospective homebuyers are having a difficult time pulling the trigger on such an expensive decision but based on predictions, prices could continue to rise making purchasing a home sooner than later more ideal. Check out the chart attached with estimates on home costs based on Freddie Mac price appreciation and mortgage rate projections.

What about Manufactured and Mobile Homes?

Overall, manufactured homes are less expensive than traditional homes. According to HomeAdvisor, their total cost is around $100-200 per square foot; in contrast, a traditional new-build home averages $150 per square foot, and can easily go as high as $400, depending on the locality.

But there’s a cheaper alternative: the manufactured home. These prefab, permanent residences are factory-built, then installed on a lot. The average sale price of a manufactured home, as of February 2022, was $128,000, according to the U.S. Census Bureau (exclusive of land cost or other expenses). Even the biggest, most deluxe models can be around $250,000.

Though traditionally associated with temporary housing and trailer homes, these days manufactured homes can be just as permanent as on-site builds. Nor do you have to sacrifice space or functionality when you live in a manufactured property. In fact, the average size home purchased is approximately 1,400 square feet, and some floor plans can exceed 3,000 square feet.

Essentially, manufactured and modular homes have become more luxurious and less expensive than traditional homes, making them a great choice in the height of economic changes that could continue to hit your pockets hard. If you are interested in learning more about the new fad in housing, you can browse for your new and customizable dream home at www.oakcreekhomes.com. Also, be sure to follow all our social media which are linked on our website.

Contact Us

Contact us today if you have more questions or would like to tour an Oak Creek Home in person. We offer 100+ Affordable Luxury Floor Plans to choose from!

Other Educational Resources

- Discover Affordable Luxury in Construction, Design, and Standard features! Plus, Take a Factory Tour and See How Oak Creek Homes are Built.

- Can you Customize a Manufactured Home?

- What Kind of Credit Score do you Need to Buy a Manufactured Home?

- Is There a Lumber Shortage in Texas?

Manufactured Home Builder Oak Creek Homes has been building affordable luxury heavy homes for over 50-years! Find your nearest Oak Creek Home Center.

The post Mortgage Rates And The Decision To Buy A Home In 2022 appeared first on Oak Creek Homes.