The Buying Process for Mobile, Manufactured, & Modular Homes

Whether you’re looking to buy a mobile home, manufactured home, or modular home right now or later down the road, we want to help you understand what the buying process looks like.

These types of homes are great for those of you who are budget-minded, looking for a starter home, downsizing, needing a ranch or lake property, or even a guest house. When it comes to buying a mobile, manufactured, or modular home, the process is a little different from buying a previously constructed single-family home or townhome. In this guide we will take a look at what this home buying process looks like by breaking it down into three parts:

- Five Steps you Need to Complete in the Home Buying Process

- Financing Considerations

- Home Site Selection and Home Site Preparation

Five Steps you Need to Complete in the Home Buying Process

Determine your Family’s Needs

Have an idea of some general features you need. How many bedrooms and bathrooms? Most mobile homes now all have at least 2 full bathrooms. Do you need a living room and family room or just a larger “great room”? What would you consider as being the key area for you in your new home? Are there special needs or considerations such as furniture size, bedroom size, special needs, etc.?

Determine a Budget

Typically lenders use a budget calculator to determine what your payment capacity is. You can find several programs online that will help you do that. A general rule of thumb is that your monthly payment will be about .8 -1% of the amount you borrow. The lenders will take into account your current debts to determine what your manufactured house payment limits are.

Choose a Builder

There are many different builders that produce a wide range of products. Some focus on building as inexpensively as possible while others concentrate on a combination of affordability and quality construction. It’s important that you have defined what your priorities are before visiting a mobile home dealership. What is on your top 5 list of features you are looking for in a home? Does the builder reflect the same construction priorities that you have identified? When you visit the dealership do you experience someone who wants to help you find your home or someone who just wants to earn a commission? Did they listen to you? What are their google reviews like? What have others experienced who have gone before you?

Find your Dream Home

Once you’ve developed your “shopping list” it’s time to have fun. When you visit your manufactured home dealership, share with them the things you are looking for. Be as detailed as possible. That will help your home consultant narrow down the search and help you find your new home sooner. Don’t hesitate to ask questions. Your home consultant should be able to help guide you through the process in a friendly, informative, and professional manner. Don’t be afraid to share information. You can’t go to the doctor and have him guess what your needs are.

Design your New Home

As NHS.com said in their post about buying a manufactured home, “The design of manufactured and modular homes has come a long way from the long, dark trailers of yesteryear. Manufactured home exteriors can match any style, from traditional ranch homes to cozy log cabins to chalets to cool coastal retreats.”

Inside – depending upon the model of your home…. You can choose paint colors, cabinet colors, and kitchen countertops. You might be able to customize some additional features as well… like adding stainless steel appliances or a farm sink and gooseneck faucet. Check out this previous post to see more on how you can customize a manufactured or modular home.

Financing Considerations

Financing a manufactured home, mobile home, or modular home is much different than financing a residential home. Here are some critical topics that you’ll need to consider when applying for a new home loan.

Credit Scores

One of the two most common questions we get is “What kind of credit score do I need to buy a mobile, manufactured, or modular home?” Great question. Most lenders have minimum scores that they are looking for. There are lenders who can work with bruised credit that is below 600 while others are looking for scores above 620 to 640. Sometimes lower credit scores can be overcome by increasing the amount of the down payment. Learn more about credit scores in a previous post here. When you talk with your home consultant it will be helpful to know where you stand in terms of credit score.

Note: Keep in mind our home consultants are not Licensed Mortgage Loan Originators. But part of their job is to help assemble the information that you need to make the application and then help the lender in collecting any other documents they may request to evaluate the application.

Down Payments

Down payments for mobile, manufactured and modular homes will depend on the type of loan and your overall credit profile. There are zero-down programs such as VA, USDA, and even a few available from non-government-backed sources. Typically, you should prepare for a minimum of 5% to start with. The down payment total won’t be called for until closing, so you’ll have some time to save a bit more.

There are Two General Types of Home Loans

Government-backed loans – FHA, VA, USDA

Non-Conforming loans – basically function similarly to private banks

- Land/home – use of land in the transaction

- Home only or Chattel loans – only consider the valuation of the home as collateral.

Government-insured loans, like HUD-backed FHA loans and VA loans, are financing options for manufactured homes or modular homes. Banks and home manufacturers offer more traditional chattel loans and mortgages to those of you at home shopping as well.

Using Land vs Home-Only Transactions

Your financing considerations will vary depending on your land situation. Do you own land, or do you need land?

You Own Land

Many people use land as a down payment for mobile, manufactured, and modular homes. Doing this can help secure a traditional mortgage and lower interest rates. In fact, oftentimes lenders can use the land equity to offset cash down payment requirements. Oak Creek Homes has done several loans with Zero Cash Down when the land equity and credit were acceptable to the lenders.

You Need Land

If you don’t have land, most dealerships can help you in locating a suitable homesite. Are you looking for private land or would it be more beneficial for you to consider a leased land option? Depending on the type of loan package, you may be able to include the land purchase into your home package (for more information see our “Should I find my land before buying” post).

Using leased land for your new home is a viable consideration. Most communities provide favorable sites with amenities that may include swimming pools, playgrounds, yard maintenance, garbage service, and city sewer services.

You can also do “home only” loans or chattel. While these loans typically have shorter loan lengths, and a bit higher interest rates, they can be a good choice because they also have lower closing costs. They keep the land “out of the deal” and only involve the land as collateral.

Securing Financing

Make a “good faith deposit” – Statistics show that presenting a good faith deposit increases the likelihood of getting favorable approval. The deposit shows your good intentions to make the purchase and also demonstrates to the lender that you have part of, if not all of the down payment on hand. Actual down payment requirements are determined by the lender based on your credit profile and the type of loan you are trying for. There are some “zero down” loans available but it’s still good to do a deposit to show good faith. That deposit can either be refunded at closing or can be applied to the loan at closing, whichever you choose. Check with your manufactured home dealership and make sure that the deposit is 100% refundable if the mobile home loan is not approved or if you change your mind.

Provide income – When you fill out the application provide accurate information on your income, detailing all sources. The lenders are looking for “pre-tax” figures. If you are paid overtime you will list that amount separately from your “regular” pay. Usually, to be counted, overtime must have been earned for at least 2 years prior.

Supply all documentation needed – Documentation is KING: Lenders will want you to provide different documentation. Expect to provide your last 2 years of w2s, 2 months’ worth of pay stubs, 3-months’ worth of bank records, copies of SSI awards letters or pensions, and a copy of the deed or land lease. Additionally, the bank may ask you to provide other documents as well. While this may seem burdensome, it is an essential part of buying a home.

Shop lenders – Credit scores are usually the ones affected once you make multiple applications within a 30-day period. I usually suggest that you approach at least 2 different lenders so you can get a comparison of offers. Things to consider when you review your lender response are terms of the home loan, interest rate, and fees. Sometimes it makes more sense to look at loan offers with lower loan fees even if the rate is higher. See a full list of lenders we work with here.

Determine your payment – I know a common question, “What will my mortgage payment be?” You can use a general rule of thumb when estimating what your payment will be. Your mortgage payment amount will be a result of 3 factors.

- Credit scores

- Amount of down payment

- Term on the loan – how long is the loan for?

Here is a calculator that can help in determining your payment

Calculate Payments

Again, be mentally prepared to provide additional documentation that the lender may require. Understand that your manufactured home consultant is not the bank, but they are there to help expedite the process.

Home Site Selection and Home Site Preparation

Let’s review what considerations come into play during the home site selection and home site preparation processes for your mobile, manufactured, or modular home.

Site Selection for Mobile, Manufactured & Modular Homes

When considering a home site location be sure to check on any local zoning or deed restrictions. Some home sites that are within city limits may require modular construction standards to meet city code for single-family dwellings. Oak Creek builds a wide range of modular home plans that meet local construction codes for single-family dwellings.

Site Preparation for Mobile, Manufactured & Modular Homes

Once you’ve found your land, here are some items you need to consider while preparing your mobile home site.

Note the lay of the land. When you are doing site prep for a mobile home, you’ll want to take note of any obvious indications of where the drainage may occur. You do not want to put your home in a low-lying area that could allow for water to accumulate under the home.

Note any obstacles that may make delivery more complicated. We suggest that you walk the property and get several different vantage points. Are there any trees or other natural features that may affect the placement of the home?

Check on “set back” requirements. Knowing how far from the property lines you have to place your mobile home can avoid costly mistakes.

Determine what utilities need to be installed. Does your selected home site already have water, sewer/septic, and electrical available? If your selected home site does not have all of these available – does your modular home dealer provide these general contracting services in addition to the cost of the home? Or will you have to secure those services outside of your purchase agreement? Be sure that the bids are from contractors who have the proper licenses and approvals to do the work in the area where you are putting your home.

Will you need a foundation? Some lenders do not require a concrete foundation as part of the home package while others do. Modular houses will always require an engineer designed and inspected foundation. It’s recommended on all of our double-wide section homes. In the State of Texas, any new manufactured home that is wider than 16’ and going on private property requires a “home pad” to be installed to help insure proper water drainage.

Have a home site inspection. It’s a good idea to have your mobile home dealer do a physical site inspection at your proposed location to help identify any setup or home site preparation issues beforehand.

Check the dealership’s policy for set-up inspections. Here at Oak Creek Homes, we have decided to use an independent 3rd party engineering firm to inspect all installations of multi-section homes. Each installation must pass a detailed 47-point inspection. What does your dealer do?

Choose skirting and underpinning, steps, and decks. What type of skirting will be put on your home? You have a wide range of choices including vinyl, metal, hardboard, masonry, or other manufactured products. Some lenders have different requirements so be sure to check with your modular home dealer about what you are getting.

Summary

We hope this guide has helped to educate you on the home buying process for mobile, manufactured, and modular homes.

Still Have Questions?

Our friendly team members would be happy to talk with you. Feel free to contact us to schedule a visit or tour.

Contact us

Additional Educational Resources

- 8 Things to Consider when Choosing a Manufactured Home Builder.

- 19 Questions to Think About Before Buying a Manufactured Home.

- Discover Affordable Luxury in Construction, Design, and Standard features! Plus, Take a Factory Tour and See How Oak Creek Homes are Built.

Manufactured Home Builder Oak Creek Homes has been building affordable luxury heavy homes for over 50 years! Find your nearest Oak Creek Home Center.

The post Mobile, Manufactured, & Modular Home Buying Process: A Complete Guide appeared first on Oak Creek Homes.

Building Cost

Building Cost

How does inflation influence mortgage rates? Inflation and mortgage rates go hand-in-hand. When inflation happens, the value of the dollar increases reducing purchasing power directly causing mortgage rates to increase. When inflation increases, people will also start to see prices increase and this fact remains the same for homes.

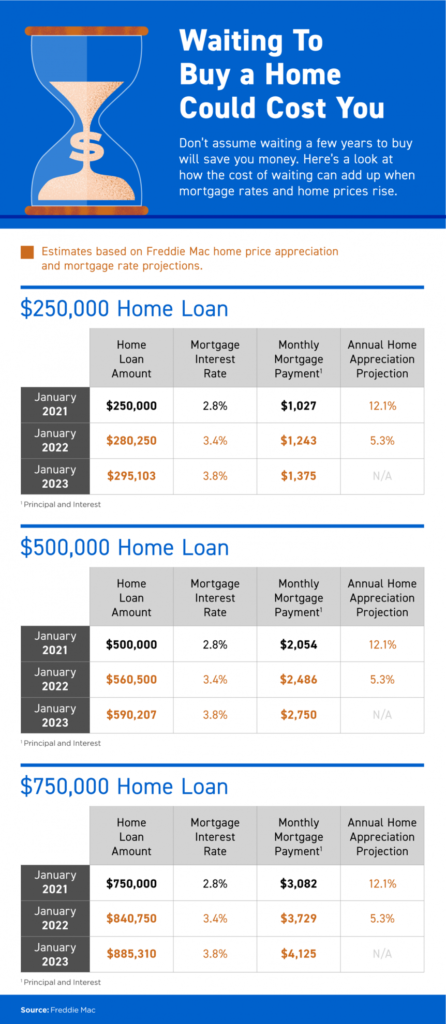

How does inflation influence mortgage rates? Inflation and mortgage rates go hand-in-hand. When inflation happens, the value of the dollar increases reducing purchasing power directly causing mortgage rates to increase. When inflation increases, people will also start to see prices increase and this fact remains the same for homes. With rates being so high, families interested in purchasing a home are reconsidering based on affordability. Rising interest rates could raise your monthly mortgage payment and even fixed mortgage rates are more expensive. To put things into perspective (according to figures from NAR) a $429,000 house will cost an additional $5,640 per year. These additional costs are not small and prospective homebuyers are having a difficult time pulling the trigger on such an expensive decision but based on predictions, prices could continue to rise making purchasing a home sooner than later more ideal. Check out the chart attached with estimates on home costs based on Freddie Mac price appreciation and mortgage rate projections.

With rates being so high, families interested in purchasing a home are reconsidering based on affordability. Rising interest rates could raise your monthly mortgage payment and even fixed mortgage rates are more expensive. To put things into perspective (according to figures from NAR) a $429,000 house will cost an additional $5,640 per year. These additional costs are not small and prospective homebuyers are having a difficult time pulling the trigger on such an expensive decision but based on predictions, prices could continue to rise making purchasing a home sooner than later more ideal. Check out the chart attached with estimates on home costs based on Freddie Mac price appreciation and mortgage rate projections.

What is petroleum? Petroleum is crude oil and other liquids produced from fossil fuels that are refined into petroleum products.

What is petroleum? Petroleum is crude oil and other liquids produced from fossil fuels that are refined into petroleum products.